"All Along The Watchtower, Bernanke Kept his View"

Dylan wrote it, Hendrix covered it immediately, Matthews reprises it in 1999. Bernanke could be listening to one of the three versions (below) on his I-Pod. The allegory is simple and yet likely to ignored again in a few more years.

I like the Chairman a lot. I like what he's done and how he's done it. In fact, he may have done a wee bit too much too early, but I'll let you decide that in a month or two.

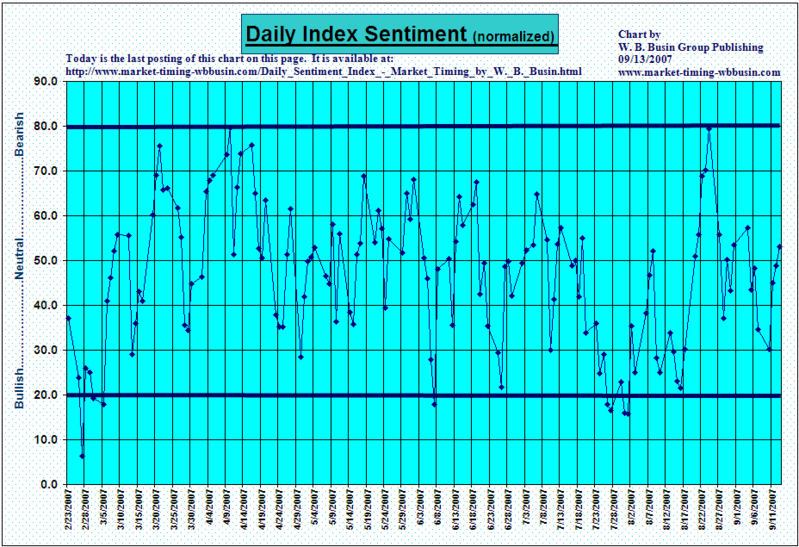

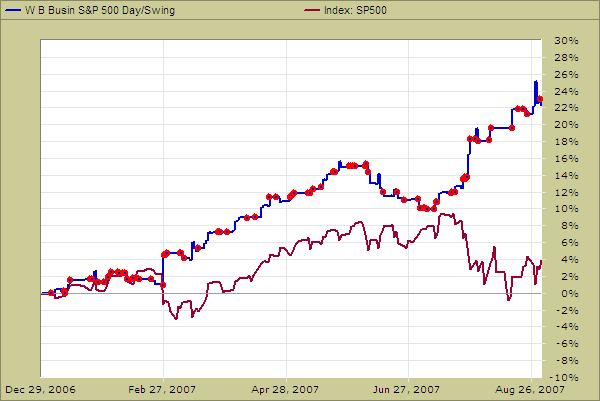

I'm bullish, very bullish - beginning in October this year. We have been discussing the correction since May. Would it be 1987 or might it be 1998? The 1987 pattern dissolved as the 1998 pattern came to prominence, and a grand scheme it has turned out to be.

So far, Bernanke has shown an understanding of the difference between who's in the quicksand, and those who feel like they are being pulled into the mire. He knows that those who feel pulled toward the mire are holding onto the rope of rescue for the rotter in the quicksand. Let go of the rope! But have mercy on his soul.

Bad lending policy makes for bad lenders making bad loans to bad borrowers. Is that news to anyone? Lenders should suffer their consequences, just as the hedge funds, who played the high risk game, and their investors should as well. This isn't a child's game where everyone goes home unscathed. Market battles are vicious to the ignorant or the blithe.

While the residential lenders gluttoned on huge fees, as they lent the public's money to the 'thieves', they ignored the late hour for affecting a rescue or a change.

All the warnings and signs have been re-told throughout the long history of 'mad money' woes. From tulips to silver to bundled mortgage derivatives, the jokers always think it's different this time. It will go on forever. It doesn't, does it. Tulips are $5 a dozen, right?

The results are always the same. Pleas for help are barely heard because the glutton's belly is still so full of the rot he's trying to digest. The gastronomic pain is so severe, he can hardly utter a whimper. But the tears flow, the hand is waves a third time as the rotter's head slips silently below the mire. No, that wasn't Bunyan's Christian ridding himself of his heavy bundle to escape the mire.

Why should they be rescued? They knew what they were doing. They lent long (interest only) by borrowing short (commercial paper). They lent to the most obese of borrowers wearing "Do Not Resuscitate" medic alert bracelets. It's difficult to say who are the greater gluttons, the lenders or the rotten borrowers.

When did you learn this most basic of market lessons that extended markets correct extensively? I learned it in 1974 and never forgot it. Ever. A day does not set the sun that some sense of 1974 creeps to the front and calms the trigger finger. It often whispers, "Patience, lad, more patience. Use that trigger finger on your cup of tea for a bit."

Mr. Dylan wrote the allegorical poem (some say apocalyptic), "All Along The Watchtower", in reverse chronological order. Reading it in reverse, you may see, as I do, the symptomatic squealing of today's gored hogs in this line: "There's too much confusion, I can't get no relief. There must be some kind of way out of here."

For me, I'll take the thief's advice, "No reason to get excited." Even though life and its markets are not a joke.

This market correction is only about half over. As Harry Truman once said, "I never did give anybody hell. I just told the truth and they thought it was hell." More down to come into the Labor Day weekend low, even if the Fed is filling its injection syringe or sharpening its rate scalpels.

First downward was lead by the RUT, then it was the SPX and NYA last week. It may be the NDX's turn this time.

______________________________________

I borrowed from Mr. Dylan, and I pray I have done no damage by imposing his words over this global dyspeptic-intermediation.

Read it in this chronological way for today's lesson in the potential of apocalyptic financial economics:

"Outside in the distance a wildcat did growl,

Two riders were approaching (Sir Dodd and his knave Barney), the wind began to howl."

"All along the watchtower, princes kept the view

While all the women came and went, barefoot servants, too."

"No reason to get excited," the thief, he kindly spoke,

"There are many here among us who feel that life is but a joke.

But you and I, we've been through that, and this is not our fate,

So let us not talk falsely now, the hour is getting late."

"Businessmen, they drink my wine, plowmen dig my earth,

None of them along the line know what any of it is worth (repos, mortgage backed securities)."

"There must be some way out of here," said the joker to the thief,

"There's too much confusion, I can't get no relief."

Then the original poem:

All Along The Watchtower

Bob Dylan

album: John Wesley Harding, 1967

"There must be some way out of here," said the joker to the thief,

"There's too much confusion, I can't get no relief.

Businessmen, they drink my wine, plowmen dig my earth,

None of them along the line know what any of it is worth."

"No reason to get excited," the thief, he kindly spoke,

"There are many here among us who feel that life is but a joke.

But you and I, we've been through that, and this is not our fate,

So let us not talk falsely now, the hour is getting late."

"All along the watchtower, princes kept the view

While all the women came and went, barefoot servants, too.

Outside in the distance a wildcat did growl,

Two riders were approaching, the wind began to howl."

_______

See and listen to the guys who understood the song:

Bob Dylan

http://www.youtube.com/watch?v=Q_ncQgjIlFM

Jimi Hendrix

http://www.youtube.com/watch?v=8aUDVpHxw9c&mode=related&search=

Dave Matthews Band

http://www.youtube.com/watch?v=hcBfiob0XbM&mode=related&search=

So far, it's just the 4th phase correction since the 2004 lows. 10-year Note rates go to 3.94%, or potentially to 3.80%, before this bull market correction is over.

Watch the EUR/JPY and USD/JPY for believable signals, like Yen down, then stocks are likely to rise.

With more downward action to come, we are preparing to buy the lows.

Join us if you want.

W. B. Busin

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}